CONRAD PRABHU

MUSCAT, SEPT 26

Despite incrementally rising personal and household indebtedness in the Sultanate of Oman, sizable sections of the population continue to exercise encouraging levels of prudence in managing their finances, a national survey by the Central Bank of Oman (CBO) has found.

The survey — part of the apex bank’s ongoing efforts to promote financial literacy in Oman — was aimed at gauging financial awareness, attitudes and behaviours. The exercise shed light on how the public approaches financial planning, saving, spending and investing, providing a snapshot of the current financial culture, the Central Bank noted in its newly published Financial Stability Report 2025.

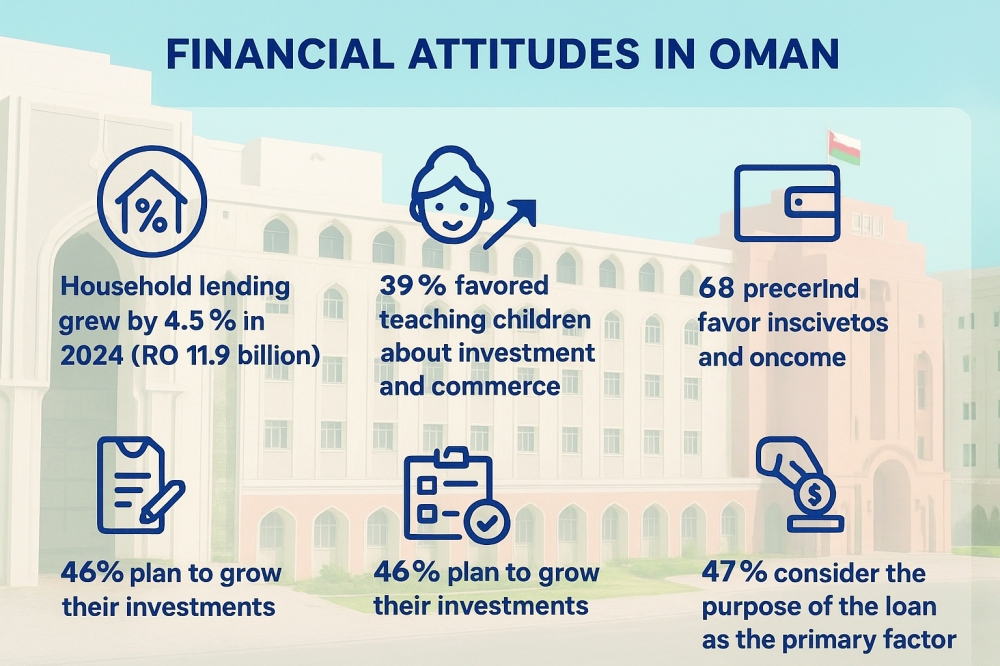

It comes as lending to households grew by 4.5 per cent in 2024 (up from 4.8 per cent in 2023 and 2.8 per cent in 2022) to reach RO 11.9 billion, representing a sizable 36.9 per cent of total bank lending for the year.

Relative to non-oil GDP, household indebtedness increased to 42.6 per cent in 2024, up from 41.1 per cent in 2023 — a trend that has remained broadly consistent with historical annual averages.

A notable finding from the latest survey relates to strong advocacy for early financial education, according to the Central Bank.

“The results show that around 39 per cent favoured teaching children about investment and commerce, while 36 per cent preferred giving weekly allowances to encourage budgeting and responsible spending. Other suggestions included opening savings accounts for children or offering money only when needed. These views reflect a clear interest in preparing children for real-life financial responsibilities through practical learning approaches”, it stated.

A large majority of respondents (67 per cent) strongly agreed that higher income enhances financial security, with another 23 per cent somewhat agreeing. Yet, the survey underscores that income alone is not considered sufficient — effective budgeting and financial planning are equally important. Despite this recognition, only 58 per cent have a financial emergency plan, while 32 per cent do not and 10 per cent have never considered one, pointing to a need for greater awareness around building financial resilience.

Respondents identified diverse financial priorities for the year: 46 per cent intend to grow their investments, 30 per cent plan to pay down debt and 24 per cent hope to buy property — reflecting an increasing focus on wealth-building and long-term stability. Borrowing decisions also appear measured, with 47 per cent saying the loan’s purpose is their top consideration, ahead of factors like interest rate, loan size and tenure — suggesting a more responsible approach to debt.

When asked how they define financial success, 45 per cent cited achieving specific goals, 30 per cent pointed to higher savings and 25 per cent emphasised debt reduction — indicating a goal-driven mindset. In scenarios involving extra income, 40 per cent said they would split a bonus between debt repayment and investment, 37 per cent would clear debt entirely and 23 per cent would invest it all. Similarly, if they received RO 10,000, 60 per cent would divide it between savings and business investment — showing a preference for balanced, cautious decision-making.

Savings behaviour, however, remains uneven: 56.7 per cent save regularly, but 25.9 per cent do not, leaving them exposed during financial stress. Budgeting remains a weak spot: while 47.3 per cent prepare monthly budgets, 23.1 per cent don’t budget at all, increasing vulnerability. Most track spending via SMS alerts (41.4 per cent) or manually (22.5 per cent), with just 14.2 per cent using apps — highlighting opportunities to promote digital financial tools.

Finally, limited income remains a key barrier, as many earn under RO 1,000 monthly, restricting access to advanced financial products. Moreover, when seeking advice, 45 per cent still rely on family members for guidance on housing or personal loans, with minimal use of professional advisory services — suggesting room for broader financial literacy and advisory outreach.

“Overall, the survey revealed encouraging signs of prudent financial attitudes in Oman. Nearly 40 per cent of individuals consistently allocate income towards emergencies, an equal share focus on long-term financial goals and 46.3 per cent actively avoid borrowing beyond their means. Together, these behaviours reflect a cautious and forward-thinking approach to money management among the population”, the Central Bank concluded.

Oman Observer is now on the WhatsApp channel. Click here