We have all heard about the abrupt failure of the Silicon Valley Bank (SVB) in the US, so soon after the year end and after receiving a clean bill of health from its Auditors. Originally the bank’s depositors were facing the prospect of losing their deposits until the FED stepped in and provided a safety net.

The problem at SVB was not complicated, it was simply an almighty bet that went badly wrong. Basically, the management decided to accept $190bn of short-term customer deposits and invest most of them in long-term fixed rate securities, with Shareholders Equity of just $16bn to cover for any potential losses.

When the FED initiated its program of raising interest rates to combat inflation, the income from the fixed securities did not change but the cost of the deposits followed the upward path of the FED interest rates. This is a classic example of poor/inappropriate interest rate risk management and is typically referred to as collecting pennies in front of a steam roller.

It turns out that management even awarded themselves generous bonuses for the pennies they were collecting – then bang, the rest is history.

Whilst the SVB does not have a branch in Oman many people have asked me if, in the current environment of rising interest rates, the same fate could behold any of the Oman banks. In order to answer this question, we need to look at two factors. The first factor is the exposure to rising interest rates and the second is the adequacy of capital should any bank incur such losses.

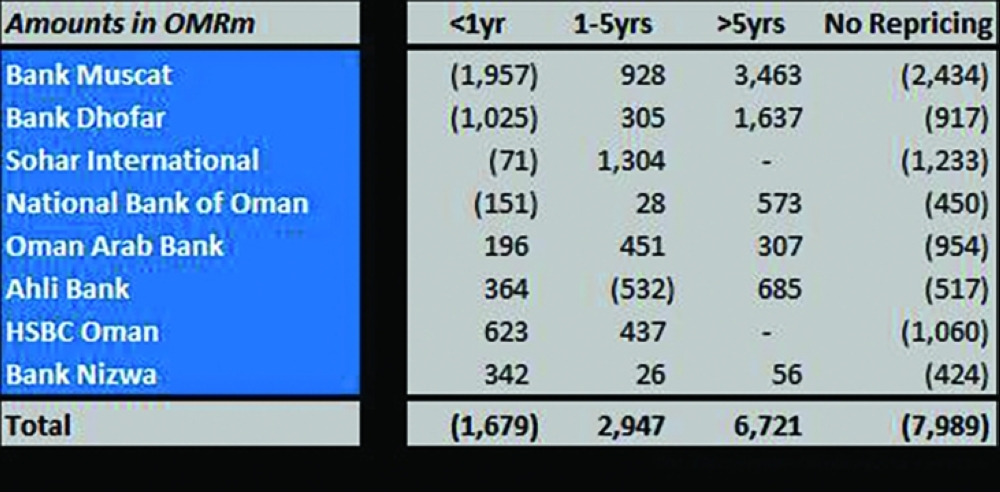

Fortunately, both of these factors are duly disclosed in the publicized annual financial statements. Moreover, whilst some risk exists in Oman, it is not in the same league as SVB and it is related to commercial lending activities of the two largest banks where the funding of long-term assets is one of the important key intermediary activities that banks undertake within any economy.

Looking at the Oman banks disclosures of their sensitivity of assets and liabilities, overall, we see a fair balanced match of repricing short-term assets with liabilities and for the banks that have longer term repricing assets, these are covered substantially by liabilities and shareholders’ equity that have no repricing terms, to keep the risk within tolerable levels. Thankfully, what we do not see is entirely speculative investments into long-term non-commercial assets.

Another potential anomaly unique to Oman that needs to be carefully watched is the CBO imposed 6% ceiling on lending to the retail sector, including housing loans. With the CBO repo rate (i.e. emergency borrowing rate) now reaching 5.5%, retail lending becomes less attractive to the banks.

Whilst the banks generate a large proportion of their funding from interest free savings and current accounts, they still need to pay market term deposit rates for approximately 60% of their funding.

As per data released in the latest CBO Statistical Bulletin, average USD deposit rates have risen by 2%, whilst OMR rates have remained flat. It will be interesting to see if this imbalance persists, or if the OMR rates also begin to rise (by 2%) to restore the historical USD/OMR interest rate spread.

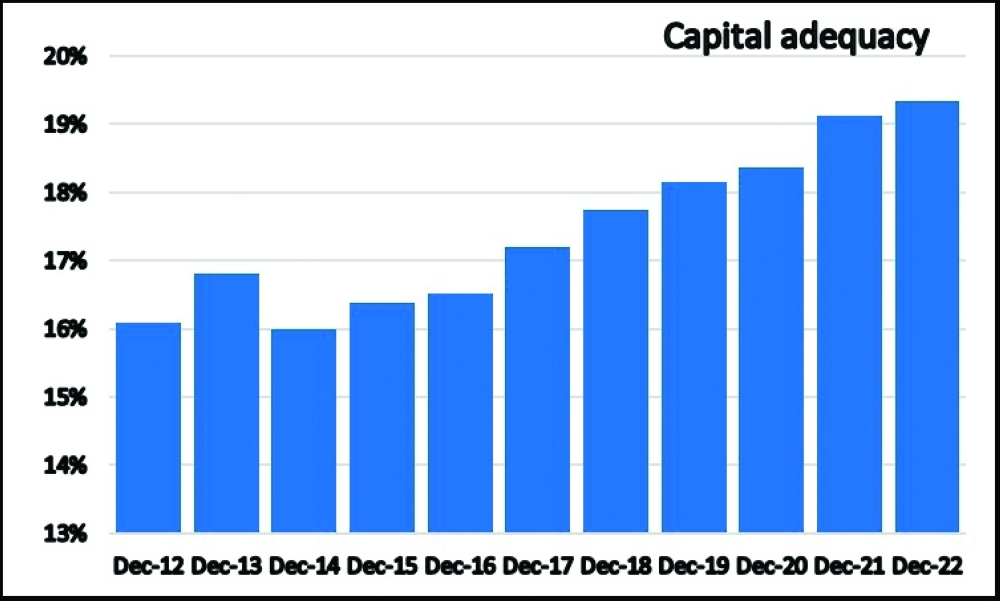

In terms of capital, we can see that the banks in Oman are very well capitalized. Under the close regulatory supervision of the CBO over the last 10 years, the banking sector has increased substantially its Shareholders Equity (from 16% to 19% of risk weighted assets), which is used to absorb losses before regular depositors get affected.

(This article was written by Karl Jackson, a seasoned Bank Risk Manager and now an Audit and Assurance Partner with Crowe Oman karl.jackson@crowe.om)

Oman Observer is now on the WhatsApp channel. Click here