STRONG GROWTH: MENA region set to add 33 GW of renewables by 2026, 80 per cent of which are in solar PV

BUSINESS REPORTER

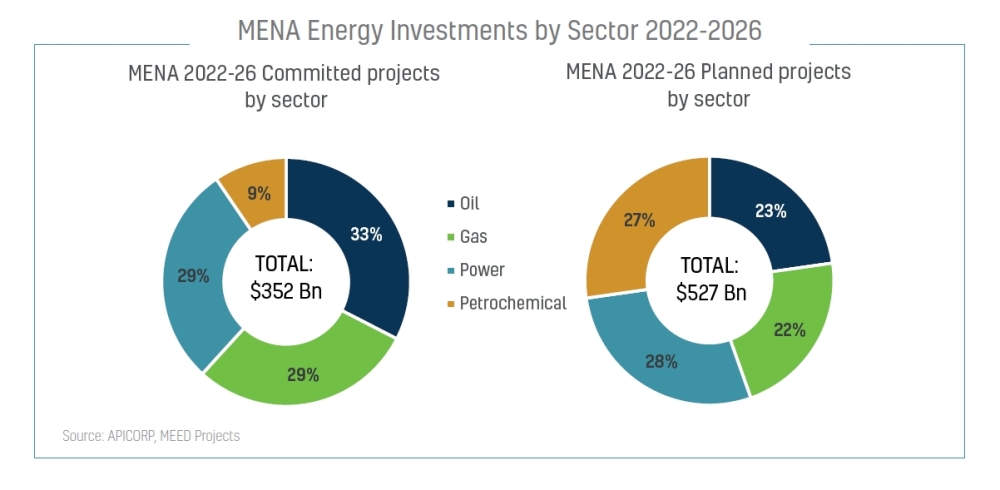

The Arab Petroleum Investments Corporation (APICORP), a multilateral financial institution, launched on Tuesday its MENA Energy Investment Outlook 2022-2026, forecasting that the total planned and committed investments in the MENA region are expected to increase by 9 per cent to exceed US$879 bn over the next five years – a $74 bn increase from the $805 bn estimate in last year’s five-year outlook.

The report notes that the Russia-Ukraine war has led to contrasting impacts on the region’s energy landscape, with net-energy exporters spearheading the increase in project expenditure thanks to the windfall of oil and gas revenues caused by the spike in prices driven by the war. However, global geopolitical volatility and macro headwinds are not curtailing oil, gas, power and petrochemicals investment growth in MENA for the upcoming 5 years.

In the GCC, committed projects comprise around 45 per cent of total energy investments – 50 per cent higher than the MENA-wide average of 30 per cent. For net-energy importers in the North Africa and Levant regions, their relative vulnerability to geopolitical risks stemming from the war compounded by the economic strains of inflation and debt burdens are beginning to show and impact energy investments.

Ramy al Ashmawy, Senior Energy Specialist at APICORP, said, “Our latest MENA Energy Investment Outlook shows that the region continues to progress in its unique energy transition path. Namely, MENA countries shoulder the largest share of global investments in oil and gas going forward to ensure global energy security and avoid an impending super cycle that may severely hamper the world economy. At the same time, the region continues to invest in decarbonisation, renewables and clean energy as part of the long-term strategic vision for a low-carbon future underpinned by a greener, more balanced, and sustainable energy mix.”

Blue and green hydrogen.

APICORP’s analysis shows that right across the region, blue and green hydrogen will dominate the emerging hydrogen markets in the near term. The report forecasts that hydrogen markets will start scaling up as the market foundations are established, and for the MENA region – GCC and North Africa specifically – the focus will be on exporting low-carbon hydrogen to demand centres in Europe and SE Asia via ammonia shipments.

Suhail Shatila, Senior Energy Specialist at APICORP, said: “In the medium term, blue hydrogen proves to be a more attractive option to the MENA region. Blue hydrogen can be produced at a relatively low cost, and it will only slightly disrupt the IOC and NOC’s existing business models. This is a central metric in the energy transition journey since hydrocarbon producers will play a key role in decarbonising the upstream oil and gas sector and help reach net-zero targets by mid-century.”

Energy Diversification

Energy diversification is at the top of the agenda, with several MENA countries integrating renewables in their generation mix as part of a shared policy objective to diversify the power mix with low-cost, low-carbon energy sources and bolster power supply security.

For hydrocarbon net-importing countries with robust renewables potential, the aim is to reduce dependence on conventional fuel imports and integrate low-cost renewables into domestic grids. Over the coming years, the priority for hydrocarbon net exporters is to free up export volumes of conventional fuels to maximise revenues at healthy price environments to fund socioeconomic development and support the decarbonisation initiatives of their respective net-zero targets.

Although few MENA countries have already pledged their net-zero targets (the UAE by 2050 and Saudi Arabia and Bahrain by 2060), electrification via renewable energy sources will be a key driver to reach those targets. However, due to the intermittency of renewable energy sources and the lack of utility-scale grid storage solutions to date, conventional fuels and nuclear will remain essential in the power supply mix.

Oman Observer is now on the WhatsApp channel. Click here