Oil prices edged lower last Friday, for a sixth week in a row, rattled by the spread of the Omicron variant, a US jobs report that missed expectations and as OPEC+ opted to continue hiking oil supplies.

Earlier, comments by US Fed Chairman Powell that a stronger US economy could prompt the Fed to accelerate tapering of its asset purchase program led to an oil and financial markets sell-off. Tighter monetary policy is typically bearish for commodities.

International crude benchmark Brent closed down at $69.9/bbl (-3.9 per cent w/w; +35 per cent ytd), while local crude marker Kuwait Export Crude (KEC) reached $72.9/bbl (+44 per cent ytd). Brent remains on the verge of entering bear market territory, having lost almost 19 per cent of its value since its peak of $86.4/bbl in late October.

Brent dropped 16.4 per cent in November, its worst monthly performance since March 2020, after the Omicron variant was identified against a backdrop of resurgent Covid-19 and amid moves by large oil consuming nations to coordinate a release from their strategic oil reserves (to lower domestic fuel prices). About 85 mb of crude oil in total could be released by the end of 1Q22, from the US (50 mb), India (5 mb), China (20 mb) and others.

OPEC+ held its ministerial meeting on December 2 amid speculation that it would react to the SPR releases and the emergence of the Omicron variant by pausing or even reversing the planned supply increase for January—a politically contentious move that would have irked the US especially. OPEC+ has consistently maintained that oil demand remains fragile while the virus continues to spread and that oil balances will swing into a heavy surplus as early as 1Q22.

In the end, OPEC ministers opted to continue increasing supply at the monthly rate of 400 kb/d but also gave themselves the option of adjusting production on the fly should oil demand weaken—the OPEC communique referred to the meeting remaining “in session”. The OPEC+ move was welcomed by the US, and members keen to continue ramping up supply were also satisfied. Moreover, the actual supply increase may fall short of target due to supply outages and capacity constraints among some members.

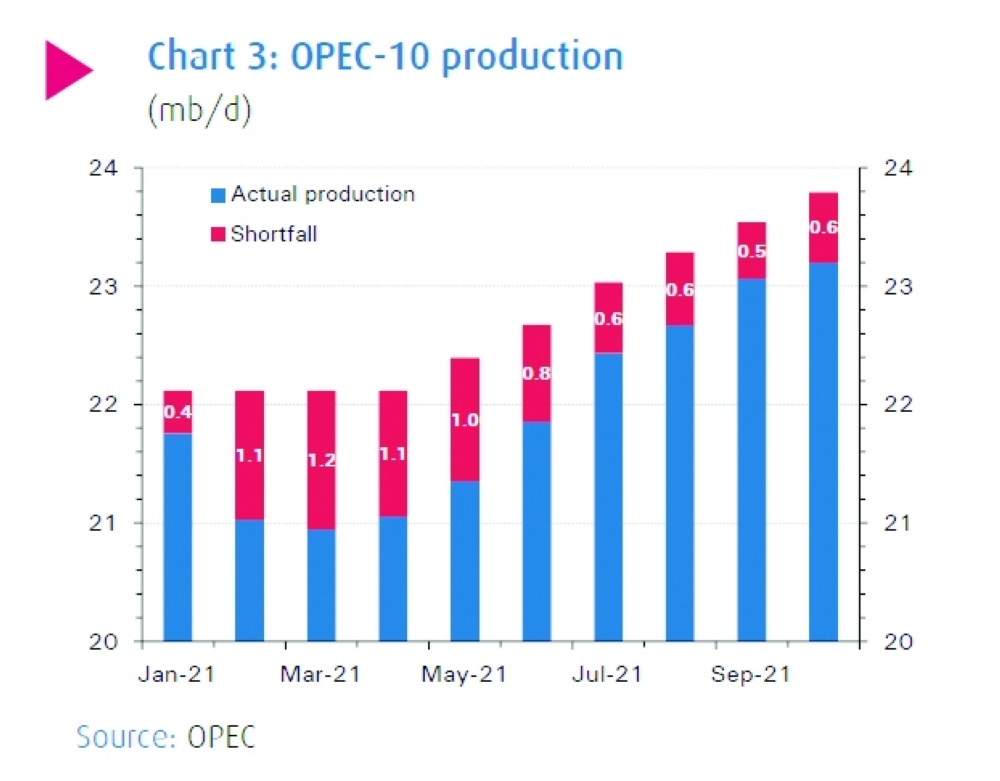

OPEC’s base case estimate of demand-supply balances in 2022 show stock builds every month and a hefty 3.8 mb/d gain in March. This scenario does envisage, however, a significant q/q decline in oil demand in 1Q22 of 1.5 mb/d, which appears extreme even accounting for both pandemic-induced and seasonal demand weakness (it is also almost 1 mb/d below the International Energy Agency’s estimate). The forecast also assumes all OPEC+ members fulfill their quotas, which is optimistic given the underperformance seen so far due to supply outages etc. In October, the aggregate OPEC-10 supply shortfall was almost 0.6 mb/d, according to OPEC secondary sources.

Outside of OPEC, the main supply impetus is provided by the US, where, as of end-November, crude production had reached 11.6 mb/d, a rise of 500 kb/d in two months, according to Energy Information Administration data.

As 2021 draws to a close, the Omicron variant has introduced more volatility into the oil market, though it is too soon to gauge the impact on oil demand.

In terms of supply, the impasse on Iran’s nuclear programme means the timeframe for the return of its oil has been pushed back, simplifying matters a little for OPEC+, which can focus on adjusting supply to demand-affecting events.

[Credit: NBK Economic Research Department]

Oman Observer is now on the WhatsApp channel. Click here