Karl Jackson

As the MSM-listed SAOG companies have all now reported their preliminary unaudited full year 2020 results, we are able to gauge the financial impact the Covid-19 pandemic is having on the Oman economy.

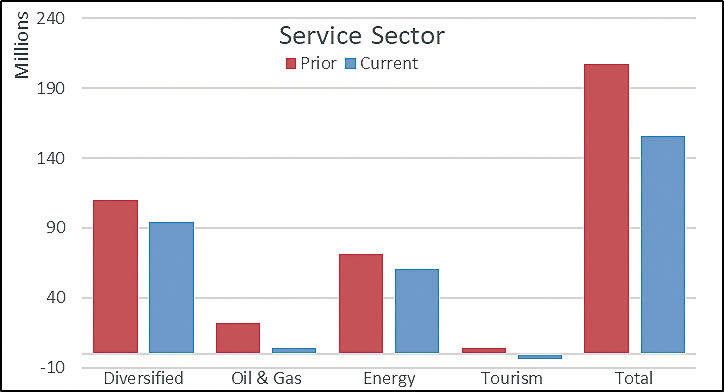

Overall, the picture is much as expected, as we see almost all the sectors down when compared to the prior year. However, five sectors that are interestingly worthy of special mention are Banking, Construction, Oil and Gas, Telecoms (included within Diversified Services) and Insurance.

In all economies, the Banking sector has exposure to all other sectors, so is the best universal barometer, as they book provisions in advance of expected credit losses (IFRS 9 ECL). This sector alone is down 33 per cent.

Another sector that is central to the Oman economy is Construction, which has not only shown a reduction, it has gone from a profitable RO 3m to a RO 23m loss position. The large construction firms, as we all know, are just the tip of the iceberg, as their activities are felt throughout the economic chain and particularly deep into the private family groups as well as the SME sectors.

Another sector that has been hit hard is Oil and Gas. With lower economic activity, less cars on the roads and the lack of air traffic requiring aviation fuel, this sector, which includes the Shell, Oman Oil and Al Maha petrol stations, saw an 80 per cent reduction in their combined profits.

Telecoms (Omantel and Ooredoo) have surprisingly also suffered with a drop in profitability of 22 per cent. With the increase in working from home and general social usage of the internet, it would be intuitive to expect this sector to have benefiting from the pandemic.

However, unfortunately their revenue base is largely fixed as they charge per month but their cost base is variable, as they must pay based on usage, which has skyrocketed.

The final sector worthy of special mention is Insurance, which has surprisingly bucked the trend and reported a 37 per cent increase in profitability. If we look at all four quarters, we see a consistent year-on-year 1st quarter before the pandemic effect took hold and annual premiums were collected.

Then in the 2nd quarter, the performance improved considerably as the lockdowns reduced activity, so there were significantly lower claims to be paid.

However, in the 3rd and 4th quarters, a slowdown ensued as new business dried up, with lower economic activity, cost cutting and an exodus of expats impacting adversely on the renewal of motor insurance policies.

We have not mentioned the Tourism sector including Airlines and Hotels, which have seen their revenues evaporate completely, only because few of these are listed on the MSM in Oman.

With the Covid-19 vaccination programme picking up pace, 2021 promises to be a year of growth as the economy and companies within it make up for the lost year of 2020.

Where survival was the word on everyone’s lips in Oman, where GDP is projected to record a contraction of close to -10 per cent. The Government and the wider business community should already be positioning themselves to rise to the challenge and potential that lies ahead.

[Karl Jackson is an Assurance and Advisory Partner at Crowe Oman with close to 30 years of audit, accounting, banking and risk management experience; email: karl.jackson@crowe.om]

Oman Observer is now on the WhatsApp channel. Click here