By Chris Midgley

On Friday, Open Interest was 108 MMB. Why so much open interest? This was most likely traders seeing value in buying Nymex WTI May-June spread at -6$/bbl, a king’s ransom for a month’s storage! On tonight’s settlement this had blown out to more than a $50/barrel negative spread, so arguably, if you can find a way of renting someone’s tanks for a quick in-out you would do this. While most futures traders will be unable to take deliver we may see a record amount committed at expiry tomorrow. Cushing is only 70 per cent full right now, so along with those who were short the contract today, some operators could make a lot of money if they can take delivery, but those caught long have taken what could be as much as a $0.5 billion bath!

After hours May NYMEX WTI has already retreated to negative $14/barrel and we’d expect this to narrow back in while the June contract should roll down. However, today, Dated Brent priced at 19.09 and ICE is about $26/bbl despite the 10 per cent sell off on ICE, which still remains relatively strong; and in our mind, Brent and June WTI still need to fall a little further to force more curtailment of production and balance the market effected by the collapse in demand due to Covid-19.

Other notations:

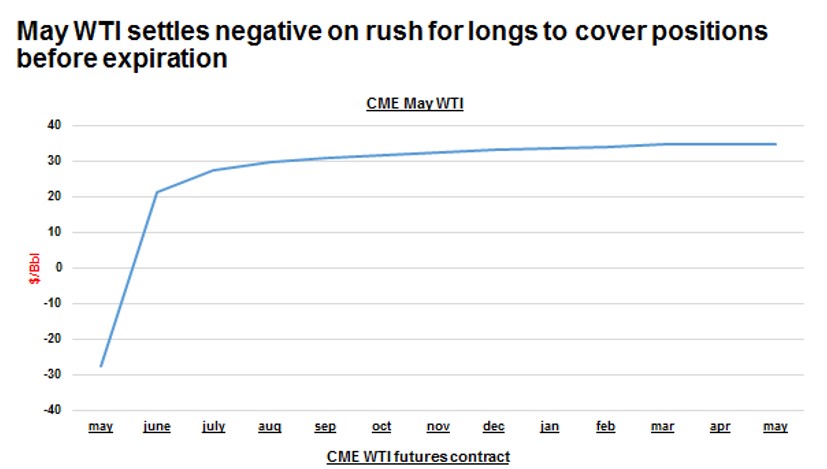

May WTI settled on Monday at NEGATIVE $37.63/Bbl, with limited liquidity and with offers chasing bids in a vacuum. Undoubtedly, one of the most volatile days in the history of oil pricing, considering that as of Friday, the May WTI futures contract settled at around $18.50/Bbl.

- Open Interest on May WTI as of Friday’s close was around 108,000 contracts for positions to be unwound or to go into a delivery process (which normally does not exceed 3,000 contracts) in 2 days (today and tomorrow). For each long futures contract there is a correspondent short contract.

- With May WTI weakening during the day, longs without capacity to receive physical delivery in Cushing were forced to liquidate their length in order to avoid delivery, causing this incredible selling pressure amplified by the absence of bids.

- The market will adjust and WTI will not trade at negative prices generally. This event is totally related to the current contract expiration.

- However, Platts Analytics outlook is for global crude supply to rapidly fill available storage onshore and afloat. As that happens, prompt prices will weaken further and producer takeaway will be constrained, ultimately limiting production.

[Chris Midgley is Head of S&P Global Platts Analytics]

Oman Observer is now on the WhatsApp channel. Click here